Introduction

Life insurance is one of the most critical financial decisions you’ll ever make. However, with so many options available, choosing the right policy can feel overwhelming. Should you go for term life or whole life insurance? How much coverage do you need? What riders should you consider?

If these questions leave you confused, don’t worry—you’re not alone. This DIY guide will break down the process in a simple, step-by-step manner to help you select the perfect life insurance policy that fits your needs and budget.

1. Understand Why You Need Life Insurance

Before diving into policies, it’s important to understand why you need life insurance. The right policy will provide financial security for your loved ones in case of an unfortunate event. Here are some key reasons why people buy life insurance:

- Income Replacement – If you’re the primary earner, life insurance ensures your family maintains their lifestyle.

- Debt Coverage – It helps cover outstanding loans, such as mortgages, car loans, or student loans.

- Children’s Education – Provides a safety net for your child’s college expenses.

- Business Protection – If you own a business, life insurance can help with succession planning.

- Final Expenses – Covers funeral costs and any outstanding medical bills.

Knowing your why will make it easier to pick the right type and coverage amount.

2. Know the Types of Life Insurance Policies

There are two main categories of life insurance:

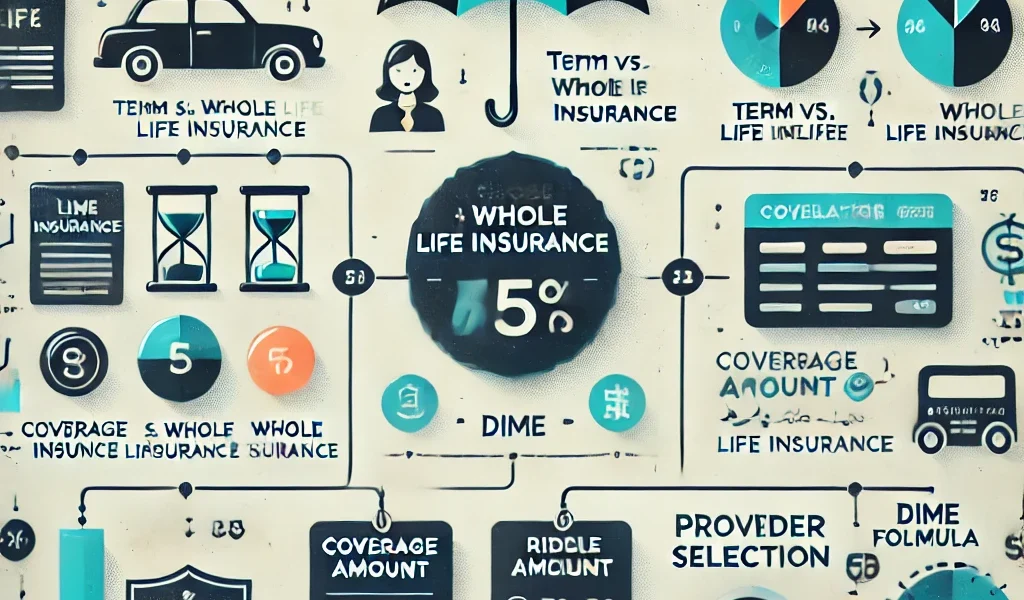

a) Term Life Insurance (Best for Affordability & Simplicity)

- Covers you for a specific period (e.g., 10, 20, or 30 years).

- Most affordable and straightforward option.

- Pays out a death benefit if you pass away within the term.

- Best for: Young families, those with temporary financial obligations (like a mortgage or children’s education).

b) Permanent Life Insurance (Best for Long-Term Financial Planning)

- Provides lifelong coverage.

- Accumulates cash value over time, which can be borrowed against.

- More expensive than term life insurance.

- Includes whole life, universal life, and variable life insurance.

- Best for: Estate planning, wealth accumulation, and those wanting lifelong coverage.

Comparison: Term vs. Permanent Life Insurance

| Feature | Term Life | Permanent Life |

|---|---|---|

| Coverage Duration | 10-30 years | Lifetime |

| Cash Value? | No | Yes |

| Cost | Lower | Higher |

| Best For | Short-term protection | Long-term security & savings |

👉 Pro Tip: If you’re young and looking for an affordable option, term life insurance is often the best choice. If you have the budget and want an investment component, consider permanent life insurance.

3. Determine How Much Coverage You Need

A general rule of thumb is to get a policy worth 10-15 times your annual income. However, you can also calculate it based on your specific needs using the DIME Formula:

✅ D – Debt: Total your outstanding debts (loans, mortgage, etc.). ✅ I – Income Replacement: Multiply your annual income by the number of years your dependents need support. ✅ M – Mortgage: Include the amount left on your home loan. ✅ E – Education: Estimate future education costs for your children.

Example Calculation:

- Debt: $50,000

- Income: $60,000 × 10 years = $600,000

- Mortgage: $200,000

- Education: $100,000

- Total Coverage Needed: $950,000

💡 Tip: Use online life insurance calculators to refine your estimate.

4. Compare Insurance Providers & Get Multiple Quotes

Not all insurance companies offer the same rates or benefits. When comparing providers, look for:

✔ Financial Strength Ratings: Choose companies rated A+ or higher by AM Best. ✔ Customer Reviews & Complaints: Check consumer feedback and claim settlement ratios. ✔ Customization Options: Some companies offer better riders and flexibility. ✔ Premium Rates: Compare quotes from at least 3-5 insurers before making a decision.

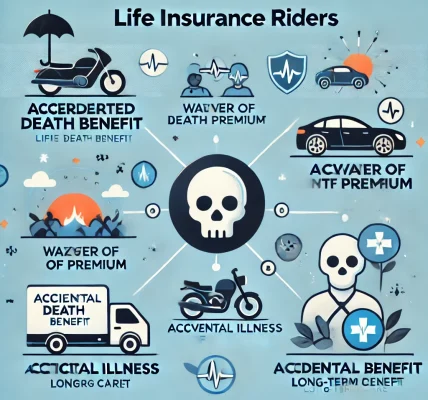

5. Consider Adding Riders for Extra Protection

Riders are optional add-ons that enhance your coverage. Here are some useful ones:

- Accelerated Death Benefit Rider: Allows you to access part of your death benefit if diagnosed with a terminal illness.

- Waiver of Premium Rider: Waives premium payments if you become disabled.

- Critical Illness Rider: Provides a lump sum if you are diagnosed with a severe illness like cancer or heart disease.

- Child or Spouse Rider: Extends coverage to family members at a low cost.

📌 Tip: While riders increase the premium, they offer valuable additional benefits.

6. Understand Common Mistakes to Avoid

🚫 Mistake #1: Only Relying on Employer-Provided Life Insurance ✔ Why? It usually covers only 1-2x your salary and disappears if you change jobs.

🚫 Mistake #2: Choosing the Cheapest Policy Without Considering Coverage Needs ✔ Why? A low-cost policy may not provide adequate protection for your family.

🚫 Mistake #3: Waiting Too Long to Buy Life Insurance ✔ Why? Premiums increase with age, and health conditions may make coverage expensive or unavailable.

🚫 Mistake #4: Not Reviewing Your Policy Regularly ✔ Why? Life changes (marriage, children, home purchase) may require policy updates.

7. Step-by-Step Guide to Buying Life Insurance

🔹 Step 1: Assess your needs (use the DIME formula). 🔹 Step 2: Decide between term and permanent life insurance. 🔹 Step 3: Get quotes from multiple insurance providers. 🔹 Step 4: Choose the best coverage amount and add necessary riders. 🔹 Step 5: Undergo a medical exam (if required by the insurer). 🔹 Step 6: Review your policy and ensure it aligns with your long-term goals. 🔹 Step 7: Purchase the policy and keep beneficiaries informed.

Conclusion: Take Action Today

Selecting the right life insurance policy doesn’t have to be confusing. By understanding your needs, comparing options, and avoiding common mistakes, you can secure a policy that offers the best protection for you and your loved ones.