Credit Card Vs Standalone Travel Insurance – which is the best ?

Introduction

When planning a trip, one of the most important considerations is travel insurance. Many travelers are unaware that they may already have travel coverage through their credit card, while others prefer to purchase a standalone travel insurance policy for more comprehensive protection.

The question arises: Which is the better option? This guide will help you understand the differences, benefits, and drawbacks of both credit card and standalone travel insurance so that you can make an informed decision.

What is Credit Card Travel Insurance?

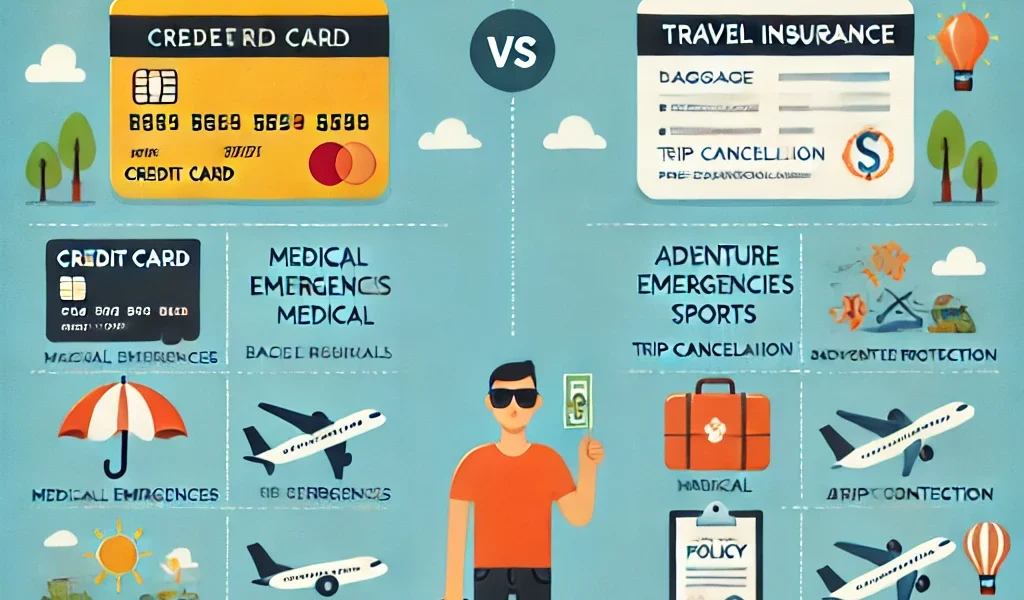

Credit card travel insurance is a form of travel coverage offered as a benefit on select credit cards. Depending on the card type and issuer, it may provide trip cancellation coverage, medical emergency assistance, lost baggage protection, and rental car insurance.

Pros of Credit Card Travel Insurance

- No Extra Cost – Coverage is included as a perk, eliminating the need for a separate policy.

- Convenience – Automatic coverage when you use the card to book flights, hotels, or rental cars.

- Basic Protections – Includes essential benefits like trip delays, lost luggage, and travel accident insurance.

- Rental Car Coverage – Many premium cards offer rental car collision damage waivers.

- Purchase Protection – Some cards cover lost or stolen items purchased during travel.

Cons of Credit Card Travel Insurance

- Limited Coverage – Medical, emergency evacuation, and adventure activities may not be covered.

- Activation Requirements – Some benefits apply only if the trip is paid using the credit card.

- Lower Claim Limits – Payouts may not be sufficient for major medical emergencies.

- Not Customizable – Unlike standalone insurance, credit card policies cannot be tailored to individual needs.

- Exclusions Apply – Pre-existing conditions, extreme sports, and non-refundable bookings may not be covered.

What is Standalone Travel Insurance?

Standalone travel insurance is an independent policy purchased from an insurance provider, offering broader and more customizable protection for travelers.

Pros of Standalone Travel Insurance

- Comprehensive Coverage – Covers medical expenses, trip cancellations, baggage loss, travel delays, and emergency evacuations.

- Higher Coverage Limits – Unlike credit card insurance, standalone policies provide higher claim limits, especially for medical expenses.

- Covers Pre-Existing Conditions – Some plans allow pre-existing medical conditions to be covered.

- Adventure and Sports Coverage – Ideal for travelers engaging in activities like skiing, scuba diving, and trekking.

- Worldwide Protection – Covers you regardless of payment method and destination.

Cons of Standalone Travel Insurance

- Extra Cost – Unlike credit card insurance, standalone policies require an additional purchase.

- Policy Comparison Needed – Choosing the right provider requires research and comparison.

- Claim Process Can Be Lengthy – Some insurers have longer processing times for claims.

Key Differences: Credit Card vs. Standalone Travel Insurance

| Feature | Credit Card Travel Insurance | Standalone Travel Insurance |

|---|---|---|

| Cost | Free (as a credit card perk) | Requires separate payment |

| Medical Coverage | Limited | Comprehensive with high limits |

| Trip Cancellation | Basic coverage | Full reimbursement available |

| Adventure Sports | Rarely covered | Available with add-ons |

| Customization | Fixed coverage | Customizable plans |

| Claim Limits | Lower | Higher limits, especially for medical expenses |

| Eligibility | Must use the card for booking | Covers all trips regardless of payment method |

Which One Should You Choose?

Choose Credit Card Travel Insurance if:

- You are taking a short domestic trip with minimal risks.

- You already have health insurance that covers international medical emergencies.

- You are booking flights and hotels with an eligible credit card to activate benefits.

- You don’t need customizable coverage for extreme sports or pre-existing conditions.

Choose Standalone Travel Insurance if:

- You are traveling internationally, especially to countries with high medical costs (e.g., the USA, Canada, Australia).

- You need higher coverage limits for medical emergencies and trip cancellations.

- You engage in adventure sports or high-risk activities.

- You want a customizable policy that suits your specific travel needs.

- You have pre-existing medical conditions that require special coverage.

Factors to Consider Before Choosing

- Destination – Some countries require travel insurance (e.g., Schengen Visa requirements).

- Trip Duration – Credit card insurance is suitable for short trips, while standalone insurance is better for long stays.

- Existing Health Insurance – Check if your health policy covers international emergencies.

- Coverage Limits – Compare claim limits for medical expenses, trip cancellations, and baggage loss.

- Type of Travel – Business, leisure, adventure, and family trips have different insurance needs.

Legal Considerations to Avoid Issues

- Read Terms & Conditions – Understand what is covered and what exclusions apply.

- Verify Coverage Activation – Ensure you meet eligibility criteria, especially for credit card insurance.

- Declare Pre-Existing Conditions – Non-disclosure may lead to claim denial.

- Check Claim Procedures – Understand how to file a claim and the required documentation.

- Understand Country-Specific Rules – Some countries have mandatory travel insurance requirements.

Conclusion: The Best Option for Your Travel Needs

Both credit card and standalone travel insurance offer valuable protections, but the best choice depends on your travel frequency, destination, and coverage needs.

- For basic coverage at no extra cost, credit card travel insurance is a great option.

- For comprehensive protection with higher claim limits, standalone travel insurance is the best choice.

- Frequent travelers may combine both to maximize benefits.