Life insurance is an essential financial tool that provides security for your loved ones. However, your health plays a significant role in determining your policy’s cost. Insurers assess your medical conditions to determine the risk level and calculate your premiums accordingly. Understanding how medical conditions affect life insurance premiums can help you make informed decisions.

1. Why Do Insurers Consider Medical Conditions?

Life insurance providers evaluate an applicant’s health status to determine the likelihood of a claim being made. Health conditions that increase the risk of premature death lead to higher premiums, while good health can result in lower costs.

Factors Insurers Consider:

- Pre-existing medical conditions (diabetes, hypertension, heart disease, etc.)

- Family medical history (genetic predisposition to illnesses)

- Lifestyle choices (smoking, alcohol consumption, exercise habits)

- Current medications and treatments

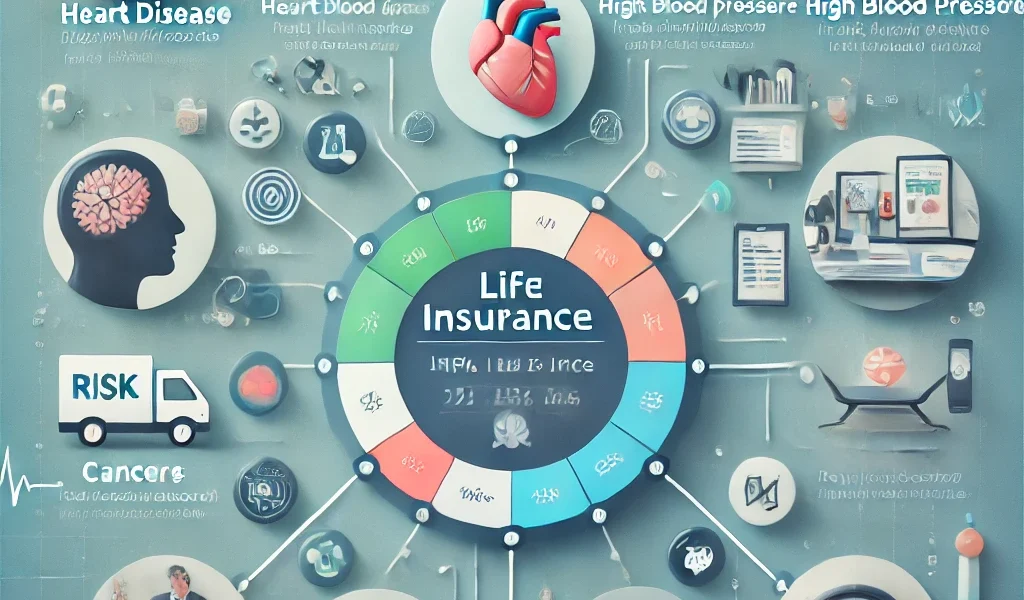

2. Medical Conditions That Increase Premiums

Some health issues are considered high-risk by insurers, leading to increased premiums or potential policy exclusions.

Common Conditions That Impact Life Insurance Rates:

- Heart Disease: Increases risk of heart attacks and strokes, leading to higher premiums.

- Diabetes: Type 1 and Type 2 diabetes affect long-term health risks.

- Cancer: A history of cancer can make it difficult to obtain affordable coverage.

- High Blood Pressure: Can lead to heart disease, kidney issues, and strokes.

- Obesity: Linked to various serious health issues, including diabetes and cardiovascular disease.

- Mental Health Disorders: Conditions like depression, anxiety, and PTSD can influence premiums, depending on severity and treatment history.

- Smoking and Alcohol Abuse: Both increase the likelihood of serious diseases and premature death.

3. How Medical Exams Affect Premiums

Most life insurance policies require a medical examination to assess the applicant’s health. The exam typically includes:

- Blood pressure readings

- Cholesterol levels

- Blood and urine tests to detect underlying diseases

- BMI measurement

- Medical history review

Applicants with unfavorable test results may be placed in higher-risk categories, leading to increased premiums.

4. No-Medical-Exam Policies: Are They Worth It?

Some insurance companies offer policies that do not require a medical exam. However, these come with trade-offs:

Pros:

- Faster approval process

- Suitable for those with pre-existing conditions

Cons:

- Higher premiums compared to traditional policies

- Lower coverage amounts

5. Ways to Lower Your Life Insurance Premiums Despite Medical Conditions

Even if you have health conditions, there are strategies to reduce your premium rates:

Tips to Improve Your Insurance Rates:

- Maintain a Healthy Lifestyle: Exercise regularly, eat a balanced diet, and manage stress.

- Quit Smoking and Reduce Alcohol Consumption: Insurers view non-smokers and moderate drinkers as lower-risk applicants.

- Control Chronic Conditions: Regular check-ups, medications, and lifestyle changes can improve health scores.

- Compare Multiple Quotes: Different insurers assess medical conditions differently—shopping around can help you find better rates.

- Consider Employer-Sponsored Policies: Group life insurance plans often have more lenient underwriting requirements.

6. How Insurers Classify Risk Categories

Insurance companies divide applicants into different risk categories:

- Preferred Plus: Best health category, lowest premiums.

- Preferred: Minor health conditions, slightly higher premiums.

- Standard: Average health, moderate premiums.

- Substandard: Higher-risk applicants with significantly increased premiums.

Understanding where you fall in these categories can help set expectations when applying for a policy.

7. Should You Still Get Life Insurance If You Have Medical Conditions?

Absolutely! While premiums may be higher, having life insurance ensures financial protection for your loved ones. Some insurers specialize in high-risk cases, making it possible to find suitable coverage at a reasonable cost.

Conclusion

Medical conditions play a crucial role in determining life insurance premiums, but they shouldn’t deter you from securing coverage. By understanding how insurers assess health risks and taking steps to improve your lifestyle, you can find a policy that offers both financial security and affordability. Always consult an insurance expert to explore your best options based on your health profile.